From Expansion to Exasperation: How Scalability Became the Consulting World’s Achilles’ Heel

Earlier last week, Bloomberg reported that McKinsey, the firm synonymous with an MBA, is laying off workers:

“The management-consulting giant McKinsey is dangling career-coaching services and nine months’ worth of pay to staffers keen on leaving the firm, the British newspaper The Times reported on Saturday. The Times reported that managers for McKinsey’s UK offices could spend up to nine months searching for a job instead of working on client projects.”

The reason:

“Some new recruits are struggling to find work. Firms are losing contracts as one-time clients slash budgets for strategic reviews amid broad cost-cutting efforts. Some employees are working long hours for the assignments they do have, while others are twiddling their thumbs. A number of firms are cutting staff by imposing large-scale layoffs or by quietly showing staff the door, citing performance reasons.”

Following a surge in demand during the COVID-19 pandemic, the consulting industry faces several challenges. During this period, companies sought consultants’ expertise to navigate the global slowdown, the shift to remote work, and the disruption in the supply chain, which led firms to increase their staff. For example, McKinsey grew significantly, currently reaching 40,000 employees worldwide (up from 30,000 in 2021).

However, as the situation balanced, businesses began to scrutinize their expenses, prompting them to scale back on consulting services. The growth forecast for the consulting market in the U.S. has been adjusted to 6% in 2024 —a significant drop from the double-digit expansion witnessed during the pandemic. According to the WSJ article, 86% of U.S. clients plan to decrease their consulting expenditures this year.

The once “reliable” source of consulting contracts from private equity work has significantly diminished, impacted by a decrease in deal-making activities as a result of rising interest rates. Typically, management consultants are used in due diligence mergers and acquisitions, followed by securing contracts to assist in the integration of companies. However, according to an analysis by Bain, the global market for mergers and acquisitions experienced a 15% decline last year, falling to a total value of $3.2 trillion.

According to the articles above, McKinsey informed 3,000 of its employees that they needed to improve their job performance. Last year, McKinsey requested its partners postpone receiving a portion of their salaries to cope with a decrease in client demand. Additionally, the company reduced its workforce by 1,400, mainly affecting those in support roles, and decelerated the rate of promotions while also cutting back on some face-to-face training and retreats.

But all of this brings me to a simple fact.

Strategy Consulting is Not Scalable

Firms like McKinsey, Boston Consulting Group (BCG), and Bain & Company are known for their rigorous analysis, strategic insight, and the high caliber of their consultants (these are our students, after all…). Despite their success and global presence, these firms face significant scalability challenges.

As a reminder, a business model is scalable if its revenues increase faster than its costs, and, usually, it fits into one of the following models:

Supply-side economies of scale or

Demand-side economies of scale.

Supply-side economies of scale are when a firm’s revenues are linear in the number of units the firm “sells” (which can be cars, widgets, or, for consulting, the number of hours it sells or customers it has), while their costs increase at a slower pace (say, square root):

This is what we’ve witnessed at Tesla, for example:

Demand-side economies of scale are when a firm’s revenue increases faster than the number of units “sold,” while their costs increase linearly.

This is what we saw with Reddit a couple of weeks ago:

The problem with the consulting industry is that we don’t see either happening.

More specifically, if we look at Accenture (one of the only publicly traded consulting firms), we can see significant revenue growth:

Which comes with a significant headcount growth:

While margins are independent of scale:

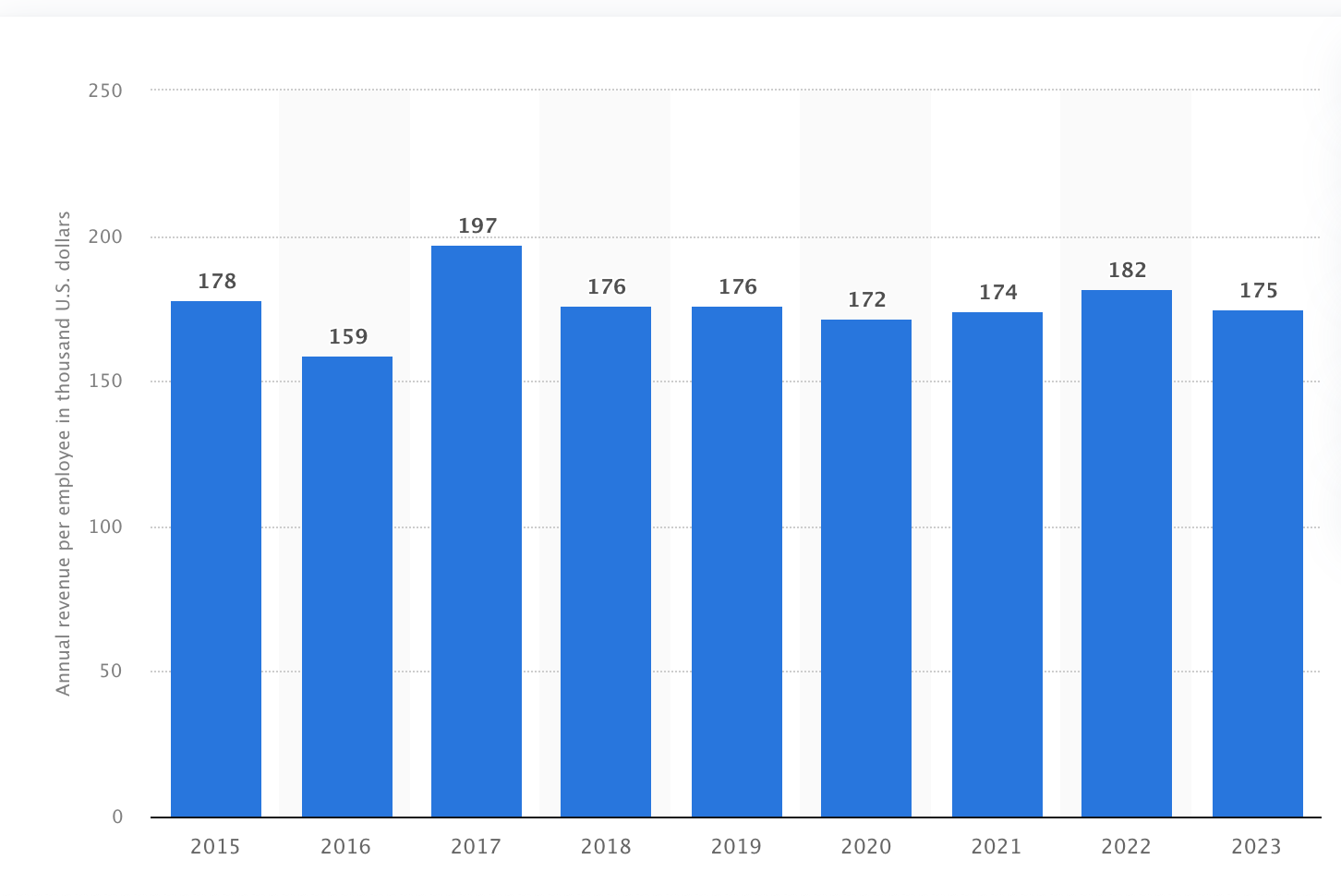

Most consulting firms are private, so gathering information over time is difficult, but if we look at the industry as a whole, we can identify a similar pattern: revenue per employee is fixed across the industry.

While there is a clear market growth:

Since the cost per consultant is linear in the number of consultants (and will potentially increase with inflation), the entire profit is extremely linear. For instance, back in 2014, consultants were making an average of $70,657 a year. Fast-forward to today, their annual earnings have risen to $78,912. This represents an 8% increase in consultant salaries over the past ten years.

Why is Consulting Not Scaling?

The core service that strategy consulting firms usually offer is highly personalized, expert advice tailored to each client’s unique challenges. So it’s apparent that this inherently limits scalability.

Unlike software companies that can distribute the same product to millions of users at marginal incremental cost, consulting services require a high degree of customization. Each project demands a team of highly skilled consultants who can dedicate weeks or months to understanding a client’s specific context, and craft somewhat bespoke solutions. This labor-intensive model means that the ability to scale is directly tied to the number of available, highly skilled consultants —an expensive and time-consuming resource to develop.

Another way to put it is that firms make money by monetizing billable hours (some of you said “meaningless decks,” but the author behind this newsletter is better than that), and the only way to sell more hours is by having more consultants.

In other words, the bespoke nature of consulting work limits the extent to which efficiencies can be realized. While administrative functions and research can be streamlined, the core service — personalized strategy development — resists standardization. This inefficiency is a trade-off for the high-value customized advice that clients are willing to pay a premium for, but also represents a barrier to scaling the business in a traditional sense.

Furthermore, consulting firms are constrained by the human capital-intensive nature of their business. The quality of their service is heavily dependent on their consultants’ talent, hence recruiting, training, and retaining top-tier talent becomes a critical priority. However, the pool of individuals with the necessary skills, education, and disposition is limited. Furthermore, the intense workload and high-pressure environment of strategy consulting led to burnout, making talent retention another bottleneck for scalability. The necessity for senior consultants to be deeply involved in projects also limits the number of engagements a firm can accept, constraining growth when the economy is booming.

In conclusion, while McKinsey, BCG, and Bain have built formidable businesses that dominate the strategy consulting landscape, their scalability is intrinsically limited by the factors defining their success.

Why Firms Need to Be Scalable

Scalability isn’t just a measure of a company’s ability to grow; it’s a crucial determinant of sustainability and long-term success.

The recent article about layoffs illustrates why firms need to scale rather than just grow.

When I teach the scaling operations course, I usually prompt students to think of a nested sequence of firms; like looking at a whole and narrowing it down to the specific sub-category you want to focus on.

At this stage, students usually ask: “Isn’t that already enough?”

Scalable firms are defined as “all growing firms that are either profitable or have a path to profitability and also have a margin expansion.” To make this more relatable, it’s like looking at all humans who play basketball, and then all humans who play basketball but also play in the NBA. And within that already selective group, all humans who play basketball, play in the NBA and have made it to the Hall of Fame.

Why am I looking for such a select group?

The examples of consulting firms above illustrate why:

Revenues can shrink rapidly due to economic downturns, shifts in client priorities, or increased competition.

Costs, on the other hand, especially those tied to retaining top-tier talent and maintaining the infrastructure necessary for delivering high-quality consulting services, are far less flexible and cannot be adjusted as quickly.

This mismatch underscores a critical business reality: unless a firm can scale (i.e., grow revenues faster than costs), it will continually need to chase new revenue to justify existing expenditures. Moreover, the adage “the next recession is always around the corner,” serves as a reminder that economic downturns are inevitable and can rapidly erode a firm’s revenue base, making scalability and the ability to adapt and grow, even more vital.

Scaling is like creating a cushion that can absorb such shocks.

Scaling is not just about expanding the size of operations, but about enhancing resilience and the ability to generate sustainable growth over time. In a world where economic cycles can turn swiftly and without warning, the ability to scale becomes synonymous with the ability to endure and last. It’s about building a business model that can not only withstand the pressures of the next recession but can thrive amidst the challenges it presents.

Can Consulting Firms Scale and Not Just Grow?

I’m not here to consult the consultants… but scaling a consulting firm involves extending its impact and revenue without a proportional increase in operational costs.

While many strategies promise scalability, their implementation can be fraught with challenges. Let’s review a few attempts to make consulting more scalable.

1. Leveraging Technology: Accenture has heavily invested in digital and cloud services, aiming to transform traditional consulting with technology. While Accenture has seen significant success, the journey has been challenging. Transitioning from traditional consulting to digital-first solutions required technological investments, a cultural shift, and re-skilling of its workforce. The lesson is that integrating technology at scale demands comprehensive strategy and commitment beyond initial investments.

2. Productizing Services: McKinsey launched McKinsey Solutions, a suite of services that productizes analytics tools and proprietary data models. While this move sought to scale the firm’s impact by offering McKinsey’s expertise in a more accessible format, the transition highlighted the difficulty of productizing high-touch consulting services without diluting the brand’s premium, bespoke advisory reputation. The challenge lies in balancing productized offerings with the expectation of tailored, expert-driven consulting.

3. Building Scalable Revenue Streams: Deloitte ventured into offering software-as-a-service (SaaS) products, aiming to complement its consulting services with scalable technology solutions. While this represents a strategic move to diversify revenue streams, it also posed challenges in aligning SaaS product development cycles with the consultancy’s project-driven model. Deloitte’s journey underscores the importance of aligning new business models with the firm’s core operational strengths and market positioning.

4. Strategic Partnerships: PwC formed an alliance with Google Cloud to bring cloud services to its clients, aiming to enhance its consulting offerings with Google’s technological capabilities. However, navigating this partnership involved aligning PwC’s deep industry and advisory expertise with Google’s technology-centric approach. The partnership demonstrates the potential of strategic alliances to scale services and highlights the complexity of merging distinct corporate cultures and operational models.

5. Focusing on High-impact Areas: BCG has made significant inroads into digital and sustainability consulting, identifying these as high-growth areas. BCG’s ventures, such as BCG Digital Ventures and BCG Green, aim to scale the firm’s impact in emerging, high-demand sectors. While BCG has positioned itself as a leader in these areas, the challenge remains in continuously adapting to rapidly evolving market demands and maintaining a leadership position in highly competitive and innovative sectors.

These examples illustrate the complexities and challenges of scaling in the world of consulting. While leveraging technology, productizing services, building scalable revenue streams, forming strategic partnerships, and focusing on high-impact areas are viable strategies for scaling, each comes with unique challenges. Successful scaling requires strategic vision, adaptability, continuous learning, and an unwavering commitment to delivering client value.

Bottom Line

The consulting industry, celebrated for its expertise in navigating businesses through challenges, has grappled with unexpected adversity.

The confluence of challenges reflects a fundamental tension within the consultancy model, which, while striving for scalability, remains inherently constrained by its reliance on human capital and the custom nature of its services. The firms’ struggles embody the harsh reality that revenue streams can evaporate swiftly, leaving fixed costs glaringly exposed and underscoring the perennial specter of economic shocks.

The current state of the consulting industry illustrates a broader phenomenon: the intrinsic challenge of scaling in a sector deeply tied to variable human expertise and customized service.

Thus, the consulting saga is a classic case of ‘the cobbler’s children go barefoot,’ where architects of business solutions face the music of Murphy’s Law— proving that even those selling umbrellas can get caught in the rain.

This is a great, comprehensive summary of the industry. Would it be correct to infer that they took the wrong signal in inferring the rise of market demand as being evolutionary rather than temporary as a result of COVID?

The other issue is that most solutions that can be “productized” by consultancies can eventually be competed away by other firms. For example, ZS Associates pioneered sales force structure models that relied on leveraging client data and intensive data processing to product optimal sales force sizing and territory structure recommendations. The combination of knowing how to structure and use client data, analytical models, and compute capacity was both unique to ZS and hard to replicate. But now you can buy software that does everything but the first and it’s often acceptable to spend 20% as much for 50-80% of the result.

I’m curious why back-end cost improvements don’t lead to margin expansion over time. All these firms have invested in automating and offshoring tasks. If billable revenue per consultant has stayed steady, why don’t costs go down over time? Is it cost inflation or something else? I would think that there is a scale advantage here where both boutique firms lack the scale to invest in and effectively manage these and clients lack the will and expertise.