From Rideshare to Robotaxi: Uber, Waymo, and the Future of Autonomous Vehicles

This Week’s Focus: The Ridesharing Revolution—Waymo, Uber, and the Future of Mobility

This week, we explore how autonomous vehicles (AVs) are transforming the ride-hailing landscape. A recent ride with Waymo’s self-driving robotaxi showcased its frictionless convenience: precise pickups, optimized routes, and no need for small talk—deeply contrasting the usual frustrations of traditional ridesharing services like Uber and Lyft.

But while Waymo’s approach—owning both its fleet and technology—challenges the network effects that have long protected market leaders like Uber, its high upfront costs and regulatory hurdles highlight the complexity of scaling AV operations. Could hybrid models be the answer? Could partnerships between fleet operators (like Waymo) and aggregators (like Uber), which combine the best of both worlds, strike the necessary balance between operational efficiency and market reach?

A couple of weeks ago, I was at the Wharton campus in San Francisco for an early morning meeting followed by a class. Usually, I stay at a hotel just a 10-minute walk from campus and walk to class, but it was pouring rain, windy, and cold. Walking meant I’d spend the rest of the day soaking wet, so I decided to call a car. But rather than booking an Uber or Lyft and having to explain why I was being “lazy” for such a short distance, I thought, why not call Waymo?

For anyone unfamiliar, Waymo is a self-driving car service that not only develops autonomous vehicle technology but also operates a fleet of robotaxis. This wasn’t my first ride in a self-driving car, but it was the first time I had one all to myself. The experience was delightful: the car arrived exactly where it was supposed to, explained how the interaction would work, and even let me choose the music. No small talk, no need to explain the short ride, and we arrived with no wrong turns, no awkward stops, and no additional instructions. Perfect!

If you use Uber or Lyft, you’ve probably experienced the friction: having to explain directions, taking unexpected routes, receiving complaints about short rides, or being dropped off on the wrong side of the street while claiming that this is the address. With Waymo, there was none of that. It was smooth, efficient, and strangely relaxing.

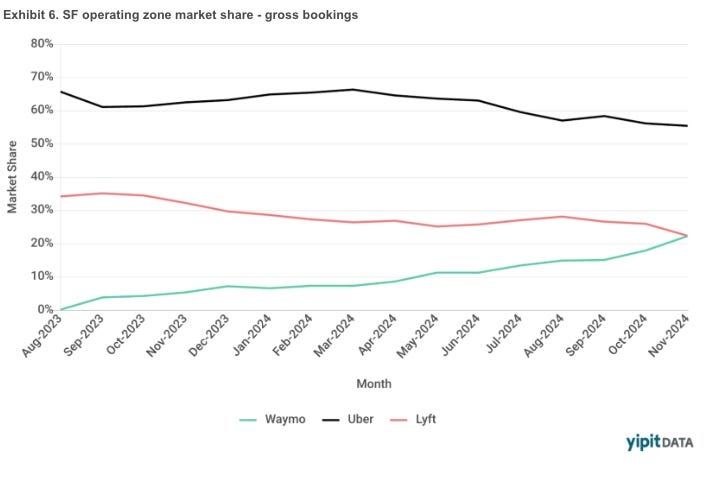

After my ride, I learned that Waymo’s market share in San Francisco is equal to Lyft’s, and is also gaining ground on Uber. This brought up many interesting questions about how autonomous vehicles are reshaping the landscape of ride-hailing services.

More specifically, how is it possible that after years of building a customer and driver base in San Francisco, a newcomer can claim market share in such a short period of time?

Are network effects not offering the promised moat?

Let’s dig deeper.

Side note: I used to write “Let’s delve deeper,” but someone alerted me that “delve” sounds like ChatGPT writes it. Scrolling back to my older articles—predating ChatGPT—I noticed that “delve” was one of my favorite ways to transition. My only conclusion is that ChatGPT was trained on my articles. The problem is that I can’t use it anymore. Thank you Sam.

So let’s dig deeper.

Network Effects Reconsidered

Network effects are often hailed as the ultimate moat for platform businesses like Uber. The more users a platform attracts, the more valuable it becomes to drivers, and vice versa. This two-sided network effect enabled Uber to scale globally and maintain its dominance against competitors like Lyft. However, the emergence of autonomous vehicles complicates this advantage in surprising ways.

To evaluate whether network effects can still drive a winner-takes-all market in the AV space, three critical conditions need to be considered:

1. Homogeneous Preferences

For a market to be a winner-takes-all (or most), customers must have homogeneous preferences, i.e., users seeking reliable, cost-effective, and convenient transportation.

2. Network Effects

In traditional ridesharing, a larger driver pool ensures shorter wait times and better service. Autonomous vehicles change the dynamic without eliminating network effects, and the advantage shifts to fleet optimization and user platform familiarity.

The figure below illustrates Lyft’s take rate over recent quarters, showing how network effects are still at play since despite losing some market share, the firm has improved its ability to extract value from its platform. This suggests that Lyft prioritizes profitability over growth, possibly at the expense of maintaining or growing its user base.

Meanwhile, Waymo, which has climbed steadily to achieve parity with Lyft in San Francisco, reflects how new entrants can disrupt established players despite strong network effects when technology and user preferences evolve.

However, the Law of Diminishing Returns applies and once the wait time for a ride drops to four or five minutes, the benefit of getting a ride in one minute is marginal. In fact, in most cases, one would argue that 4-5 minutes offers the perfect amount of time from call to meeting point! For Waymo, network effects are not about more drivers, but rather the optimal deployment of cars throughout the city. Based on my experience (which is anecdotal, but supported by the market share graph), they’re approach is effective but clearly requires significant capital, which Waymo seems to have plenty of.

Waymo’s entry hasn’t eroded the network effects for Uber and Lyft significantly, which brings me to why this isn’t (and possibly never will be) a winner-takes-all market.

3. Low Multi-Homing Costs

Multi-homing costs, or the friction associated with using multiple platforms, are minimal in the ridesharing space. Switching between Uber, Lyft, and Waymo has become trivial as the core experience—getting from point A to point B—is nearly identical. A rider’s primary concern becomes availability, price, and convenience rather than brand loyalty.

This suggests that while preferences in the ride-hailing market are relatively homogenous and network effects are still strong, the low switching costs between platforms alter the competitive dynamics fundamentally. The ease of switching significantly undermines the monopolistic potential typically afforded by network effects.

Centralized vs. Decentralized Ownership

Considering all this, we’ll probably see multiple potential models emerge. Uber’s asset-light model—relying on drivers who own their vehicles—contrasts sharply with Waymo’s strategy of owning both the cars and the underlying technology.

Waymo’s approach involves significant upfront costs: sophisticated lidar sensors, radar systems, and cameras make each vehicle a high-stakes investment. Yet, owning the fleet allows Waymo to optimize utilization and ensure reliability—crucial for a robotaxi business.

This raises questions about scalability. Centralized ownership offers consistency but limits flexibility. Decentralized ownership, such as Uber and Tesla’s vision of individual car owners leasing their vehicles to ride-hailing networks, provides elasticity but risks uneven service quality.

Siddiq and Taylor’s paper “Ride-Hailing Platforms: Competition and Autonomous Vehicles” (which I’ve mentioned before, but am so fond of the paper that I must do so again) provides interesting insights into the competitive dynamics and collaboration opportunities in the autonomous vehicle space. Their game-theoretic model investigates two scenarios: platform-owned AVs versus individually-owned AVs.

With Waymo pursuing fleet ownership and Uber focusing on platform integration, understanding the implications of these models is crucial for firms, policymakers, and labor advocates. The key question is: How does AV ownership structure (platform vs individual) impact ride-hailing platforms’ profits, agent welfare (consumers and drivers), and social welfare?

The paper develops a game-theoretic model that captures the complex dynamics between competing ride-hailing platforms. Their model incorporates several key factors: how consumers respond to pricing decisions, how labor supply (whether human drivers or AV owners) reacts to wage offerings, and how different AV ownership structures influence costs and operational decisions.

For platform-owned AVs, the study shows that when AV costs are high, platforms experience reduced profits. This occurs because the high fixed costs of maintaining an AV fleet intensify price competition between platforms, ultimately hurting their bottom lines. However, when AV costs are low, the platforms benefit from operational efficiencies while consumers enjoy lower prices, leading to improved overall welfare.

The dynamics shift notably when examining individually-owned AVs: the platforms’ profitability becomes heavily dependent on the intensity of price competition in the market. The research shows that social welfare consistently improves when individually-owned AVs enter the market at low costs, as this creates a more flexible supply of vehicles that can better match demand patterns.

These findings have interesting implications for companies like Waymo and Uber. Waymo’s strategy of owning and operating its own fleet provides greater control but carries significant risks of underutilization during low-demand periods. Uber’s approach of integrating independently owned AVs offers flexibility in scaling operations but may miss out on the cost efficiencies that come with direct fleet ownership.

One of the paper’s most interesting results is summarized nicely in the abstract:

“The structural effect of access to AVs on social welfare depends on who owns AVs. Access to individually-owned AVs increases social welfare; in contrast, access to platform-owned AVs decreases social welfare--if and only if the AV cost is high.”

If AV costs are high (as they are now), we (as consumers) are better off when we own the cars and allow the platform to use them (a model more akin to Uber). If the costs of these cars is low (e.g., if Tesla manages to get their act together both in terms of FSD and low cost), then we are actually better off with a platform owned mode (like Waymo).

Market Structure and Strategic Alliances

The research suggests that hybrid models might offer the best path forward. Partnerships between fleet operators (Waymo) and platforms (Uber) could combine the benefits of professional fleet management with efficient market distribution through established platforms. This could help optimize vehicle utilization while distributing the risks associated with AV deployment.

The future of the AV market is more complex and will likely involve a mix of collaboration and competition. Waymo’s partnerships with Uber in cities like Austin and Atlanta highlight the strategic importance of leveraging existing demand aggregation platforms. These alliances enable Waymo to maximize the utilization of its fleet while Uber maintains its position as the leading demand aggregator.

However, such partnerships are fraught with strategic tension. As Waymo’s market presence grows and it refines its autonomous fleet, the question arises whether it will continue to rely on Uber’s platform or pivot toward building its own direct consumer channel as it did in SF.

Tesla’s potential entry further complicates the landscape. Elon Musk’s vision of a decentralized Tesla Network, where individual owners lease their cars, aligns with the idea of distributed fleet ownership. However, this model’s success depends on achieving full autonomy (Level 5) and convincing car owners to forgo personal use during peak hours—a hard sell. Tesla’s focus on enabling small-scale fleet operators could reshape the competitive dynamics by introducing more decentralized alternatives to Waymo’s centralized model and Uber’s platform-driven approach.

Waymo, Uber, and Tesla must also contend with the challenge of balancing peak demand with fleet utilization. Uber’s dynamic pricing model, supported by a hybrid of human drivers and AVs, allows it to scale supply more flexibly than Waymo’s fixed fleet model. Conversely, Waymo’s control over its fleet enables it to ensure service reliability and lower operational costs in the long run, provided it achieves sufficient scale.

Furthermore, Waymo’s current partnerships with Uber could serve as a template for other hybrid models, combining the operational efficiency of AVs with the demand aggregation strengths of ride-hailing platforms. This collaborative strategy may become a necessary step to address the underutilization risk faced by standalone fleets.

The ultimate shape of the AV market will hinge on these evolving alliances, with winners likely determined by their ability to optimize utilization, manage costs, and meet diverse consumer preferences. As such, the interplay between competition and collaboration will remain a defining feature of the industry’s growth trajectory.

Lessons from GM Shutting Down Cruise

The rapid evolution of AVs also explains why one of the key players decided to exit the market. About a month ago, General Motors announced that it is shutting down Cruise as a standalone robo taxi service:

“General Motors is rethinking its robotaxi dreams, announcing yesterday that it will no longer fund the development of a dedicated robotaxi under the Cruise division. Cruise, established in 2013 and acquired by GM in 2016, has faced a tumultuous time over the past few years as it strived to put its lounge-on-wheels Origin robotaxi into production. GM said that it aims to merge Cruise and its GM technical teams into a single group to focus on autonomous and assisted driving.”

Financial Strain and Unsustainable Costs: Despite significant investments, Cruise struggled to achieve profitability (as does Waymo). High fixed costs associated with autonomous vehicle technology, combined with limited deployment and low utilization rates, made the standalone service unsustainable. GM recognized that continuing to fund Cruise as a separate entity risked further financial losses without clear paths to scalability and profitability.

Operational Complexity: Operating a robotaxi service requires substantial infrastructure, including vehicle maintenance, mapping, and customer support. These demands exceeded Cruise’s capabilities as an independent unit. Integrating Cruise’s technology into GM’s broader vehicle portfolio allows the company to streamline operations and focus on core competencies.

Strategic Realignment: By folding Cruise into its main operations, GM can leverage its manufacturing expertise to develop autonomous features for its consumer vehicles. This strategy aligns with GM’s broader vision of integrating autonomy and electrification into its product lineup, ensuring technological relevance without the financial burden of operating a separate mobility service. The cars may be used, ultimately, in some type of ride-hailing platform (say, on the Uber platform), but not as standalone provider

Competitive Dynamics: Waymo and Tesla have established themselves as leaders in the autonomous vehicle space. GM’s decision reflects an acknowledgment of the competitive challenges posed by these firms. Rather than competing head-to-head in the robotaxi market, GM aims to differentiate itself by focusing on advanced driver-assistance systems and semi-autonomous features.

Mitigating Reputational Risks: Cruise faced public scrutiny following high-profile incidents that involved its vehicles. By discontinuing the standalone service, GM distances itself from these controversies while retaining the technological advancements developed by Cruise.

The implications are clear: GM’s pivot highlights the challenges of operating autonomous vehicle services as a standalone business.

By focusing on technology integration rather than direct competition, GM aims to derive long-term value from its investments while mitigating financial and reputational risks. This move underscores the importance of adaptability in an industry where technological and market dynamics evolve rapidly.

And all this is exactly why I believe the future is more likely to be one of high cost AV’s, and why we (as consumers) may prefer individual ownership.

Conclusion: The Path Forward

A key factor, which I didn’t address is regulation.

The AV industry faces complex regulatory challenges that significantly impact widespread deployment, characterized by fragmented legal frameworks across jurisdictions. While cities like San Francisco and countries like Japan have embraced AV testing with clear protocols, others maintain restrictive policies, creating operational inefficiencies for companies attempting to scale.

This fragmentation is compounded by unresolved issues around safety standards, liability frameworks (particularly in accident scenarios involving hardware failures or software glitches), and data privacy concerns under regulations like GDPR. Cybersecurity emerges as another critical concern, as interconnected AV systems become potential targets for malicious attacks.

These challenges affect companies differently: Waymo’s geofenced approach provides regulatory advantages but may limit scalability, Uber’s hybrid model offers operational flexibility across regions, and Tesla’s vision of individual owners leasing AVs introduces additional regulatory complexities.

Waymo’s rise signals a paradigm shift in urban mobility, challenging Uber’s dominance and reshaping market dynamics. While Uber’s hybrid model—blending human drivers and AVs—offers short-term resilience, the long-term outlook hinges on how effectively it integrates autonomous supply. For Waymo, scaling profitably while maintaining service quality will determine whether it becomes a dominant player or a niche operator.

Ultimately, the AV race is not about technology but about business models, partnerships, and adaptability. As robotaxis proliferate, the question isn’t whether they will transform transportation but who will own the road. And the road is long.

The analysis is good. There is a reason Tesla is only at self driving level 2. While Waymo is at level 4. Even Mercedes Benz is at level 3. Tesla was supposed to pass Waymo in the self driving dust, even though Waymo had a 5 year head start. Tesla has over a million cars to Waymo's less than 1,000 cars on the road. That's a thousand times more data for its neural networks. But in Musk's infinite wisdom he removed radar and didn't use lidar. He said people don't use them so I don't need them. But people have a more developed neural network. He also wanted to cut costs, even though historically electronic device's costs have declined.

Intriguing analysis, but how is the situation affected by the fact that many rideshare drivers drive for both Uber and Lyft? And of course, most customers use both Uber and Lyft, and would add Waymo, when it becomes more widely available. Are there data on how many unique drivers drive for Uber and Lyft, and how many split their time between the two? In other words, is there double-counting in the estimates of the capacity of each platform?Likewise, how many riders are uniquely loyal to Uber or Lyft, and how many switch back and forth? And how big of a deal are the "frictions" that you mention (and which seem to annoy you with Uber and Lyft) to most customers -- Has anyone studied this issue? If these frictions are indeed significant to a large proportion of riders, then Waymo would offer a significant point of differentiation.