Hoka’s Marathon: The Slow Dance of Strategic Growth and Sneaker Economics

A few days ago, this year’s UTMB, the most grueling of all ultra-marathons, came to its end. Crossing the finish line is almost impossible as it’s like running four marathons back to back while ascending and descending Everest (32,940 ft, 10,040 meters, to be precise)...Impossible! The winner, however, finished in less than 20 hours, which is truly unbelievable! I’m telling you!

And that’s when the real discussion started.

What shoes was he wearing?

When asked, the answer was:

“Walmsley has two different all-black Hoka prototype shoes that he’s been training in for UTMB. Both are customized versions of Hoka Tecton X 2 shoes that include Peba foam midsoles and dual/parallel carbon-fiber propulsion plates, but each has different plate, foam and upper componentry and characteristics. The primary pair that he thinks he might run the whole course in is lighter than the prototype he wore last year, has a different outsole with bigger lugs and has more interior padding. The secondary pair of shoes looks identical but it’s even lighter and more responsive.”

This is interesting on multiple dimensions. First, regarding the changes that were triggered in the world of running, and second, considering Hoka’s growth story.

A few years ago, carbon plates were inserted into running shoes, and it created an entire list of regulations on both the stack height of the shoe and its availability.

“When seeking approval for a New Shoe, the sports manufacturer must provide information about the Athletic Shoe’s availability (i.e. where and how they can be purchased) the time limit for which must be at least one month before an Applicable Competition.”

As well as:

“New Shoes that are Available for Purchase are subject to stock (including size ranges), supply chains and manufacturing timelines. There is no obligation on a shoe manufacturer to re-stock an Athletic Shoe that has been Available for Purchase and is sold out.”

I never knew the World Athletics Organization cared about the shoe supply chain, and while Jim Walmsley’s shoes are not subject to this regulation since the UTMB is not part of the World Athletics, I’m sure we’ll see some of the developments that went into them on the market very soon.

Hoka’s Growth Story

But this brings me to the main topic of today’s newsletter: Hoka. The WSJ devoted a whole article to their unique growth strategy:

“They were big, weird, contrarian and French, and there wasn’t much reason to expect they would become huge in the U.S. In fact, when Hoka’s founders sold the company to Deckers Brands in 2012, their sales were around $3 million that year. Hoka’s sales over the past fiscal year: $1.4 billion.”

But it’s not only the numbers:

“These peculiar shoes have become the oversized sneakers of choice for people who are hardcore runners and people who have a hard time walking—athletes, nurses, restaurant waiters, postal workers, TV writers, cool teens and their grandpas. Some wear them because they want to. Others wear them because they have to. Either way, a great many of them develop a fascination and then an obsession with their Hokas, which have conquered the hearts, wallets and feet of American consumers.”

I enjoy running, and it’s one of my favorite activities to do with students, but sneakers are not really my thing. Just this Thursday, I had this academic year’s first run: a 5-mile, 5:30 a.m. run with a few MBA students in SF, but you know, an easy zone 2 run where I can talk about scaling, supply chains, and pitch my research on the consensus effects. But I am digressing.

What caught my eye in the article on Hoka was the following sentence:

“The success of Hoka was also made possible by the brand’s counterintuitive business strategy. It turns out Hoka grew fast by moving slowly. ‘Could we grow faster? Yes,’ said Caroti, Deckers’ chief commercial officer and Hoka’s interim president. ‘Is that good for the long-term health of the brand? No.’”

All right, all right, all right …

This is rare to hear from an executive at a brand with such explosive growth. The article points out that Hoka’s executives are pacing themselves and are being cautious about getting too big too soon as they realize that trying to win every single consumer is usually how a company loses its identity.

And it’s very clear that this discipline is paying off. Hoka sales amounted to less than 10% of Deckers’ revenues only five years ago. Now they account for nearly 40%, and Deckers has never been worth so much. This company is one of the few whose stock price has doubled over the past year for reasons that have absolutely nothing to do with AI. And indeed, the growth was slow. It took five years for Hoka’s sales to accelerate from less than $3 million to more than $100 million and another six to zoom past $1 billion.

It’s clear that prudence doesn’t come naturally to companies that have financial incentives to grow in the short term, and the retail industry is littered with cautionary tales of brands that overestimated their appeal, flooded stores, and lost their air of exclusivity along with their ability to command a premium price tag.

According to the article, the key to Hoka’s success was to avoid the risk of overabundance by keeping their sneakers out of the biggest big-box chains. Additionally, careful distribution and healthy reliance on direct-to-consumer sales allowed them to control pricing even when the brand was blowing up.

While this may seem intuitive, it’s not as simple as it sounds, so let’s delve deeper, as usual.

Not a Scarcity Story

The WSJ article focuses a lot on the ability to remain scarce as long as possible, but I don’t think Hokas were ever scarce, and definitely not the only shoes that experienced some scarcity.

However, there are many brands whose best-sellers are currently out of stock in most or all sizes. Try finding a Nike Alphafly, which Eliud Kipchoge ran in, and let me know how that went. Similarly, most colors and sizes of the Asics Superblast are out of stock, but I didn’t see the same growth:

“Sneaker sales grew rapidly last year — up 20% in 2021 versus 2020, according to the NPD Group — but continual supply chain issues have led to out-of-stocks.”

What drove these stockouts?

Running shoe OEMs benefited from pandemic tailwinds, like hybrid work and casual office attire, as people discovered that sneakers, which are engineered to run on trails, also worked as everyday shoes on flat roads and city streets, and with gyms closed, many people picked up running as a hobby.

On the supply side, these stockouts were caused by Covid-related supply chain issues since most shoes are made in southeast Asia and were impacted by factory closures and logistics disruptions:

“Supply chain disruptions stemming from the Covid-19 pandemic are estimated to have cost the US apparel and footwear sectors between $9bn-17bn in 2022 alone according to new data from the International Trade Commission.”

So, during the last few years, scarcity was clearly a common phenomenon for the entire industry. However, scarcity alone is not enough. So, what is it about Hoka’s specific growth strategy that was so different?

“‘The way you got your brand out there was that you had to be everywhere,’ Doolan said. ‘Today you don’t have to be.’”

And to understand why it makes sense to avoid the big channels, we must first understand shoe economics.

The Economics of Running Shoes

Ever found yourself scoring a pair of fire kicks on sale and thought, “I bet they’re still making bank off me”?

You’re not alone in wondering how much it really costs big brands to produce sneakers that have us all reaching for our wallets. It seems everyone has an opinion on the seemingly grand gap between production costs and retail price, especially when it comes to celebrity endorsements bumping up the price tag.

So, as usual, we’ve taken a magnifying glass to the whispers surrounding the high-profit margins of iconic brands.

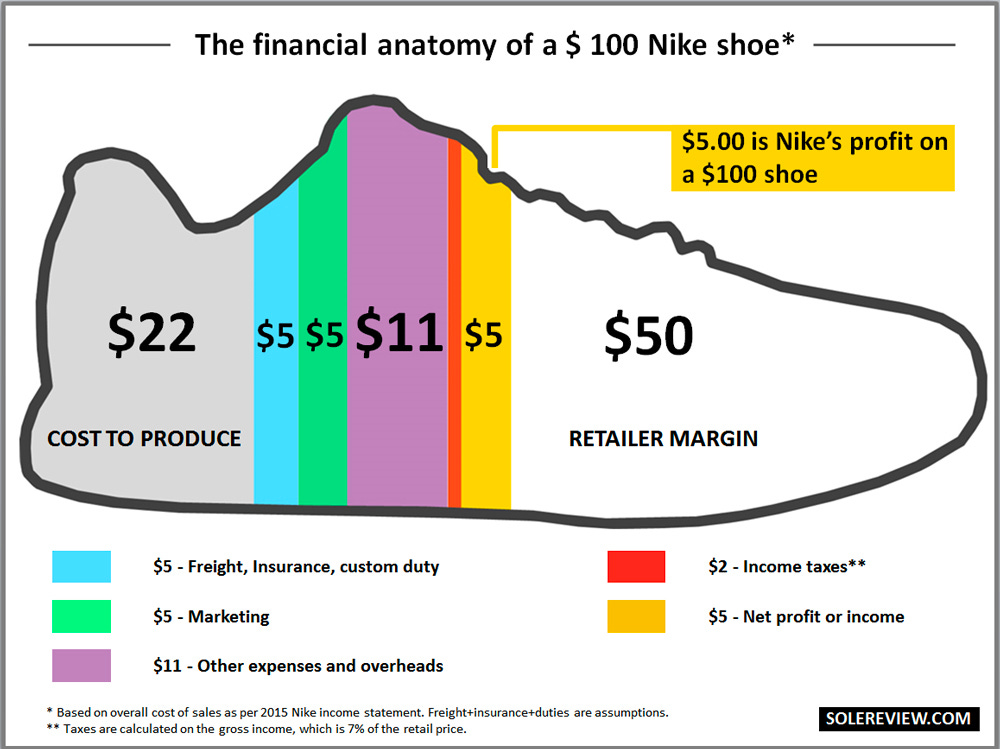

I already discussed the notion of Total Landed Cost: The end-to-end cost from factory to store. The computation below is based on numbers from 2016 for a $100 shoe:

The article puts everything in perspective for the economics of an Adidas shoe:

As well as for a Nike shoe:

Looking at the overall picture, it doesn’t seem so rosy, does it? On a pair of $100 shoes, Adidas makes a profit of only $2. Nike fares much better, making $5.

And what about the retailer?

When looking at the split here, we can see that retailers don’t make a great deal of money either, do they? For starters, it’s pretty obvious they aren’t able to sell what they bought from the brands at full sticker price.

Foot Locker’s purchase price for every sale of $100 shows up as $66 in their financial reports, and not $50. In plain terms, Foot Locker sells its merchandise for a 24% discount on average.

Given the economics, it’s evident that this is a brutal business for almost everyone involved.

Back to Hoka

So what did Hoka do differently?

“You want to be in the right places in front of the right individuals…. On its path to $1.4 billion in sales, the brand moseyed from running shops to outdoor specialists like REI to large retailers, though executives actually turned down the opportunity to move Hokas into Foot Locker before the pandemic. ‘We were not ready,’ Doolan said. People had to be familiar with Hokas before they were willing to buy Hokas. Otherwise the shoes would have been hiding in plain sight on the wall. By last summer, the brand’s awareness was high enough that it was ready for one of the country’s biggest sneaker chains. ‘We’ve held out a little bit longer than we needed to,’ Doolan said. ‘But now we’re more likely to have success.’”

While demand does play its part, I would argue that a big part of it is the economics. If the retailer takes such a big chunk of the revenue and then doesn’t have incentives to sell it (since the margins are so low), the manufacturer needs to make sure they get the right channel at the right time.

An example is Hoka at Dick’s:

“They followed a similarly conservative playbook at Dick’s Sporting Goods. ‘We started very slowly with them,’ Caroti said. ‘In fact, initially, it didn’t work.’ Hoka tested the market in a small number of Dick’s stores as early as 2014. They were uncharacteristically quick to end the experiment when they didn’t like what they found. ‘It was a bit too early,’ Caroti said. ‘There was no consumer demand.’”

Fast-forward to 2020, where Hoka decides: “Let's give it another whirl,” and starts with a shy number of 10 stores. By 2021, it added 40 more stores, and by 2022, another 100!

What’s the difference between the stores? Why choose some chains while deprioritizing others? Why start at smaller retailers first? Clearly, their mix of customers is different, but so is the quality of their service. It’s clear that buying good running shoes requires good advice from sales associates. And finding good sales associates (and I say this as a customer) has become more difficult over the years.

In her book, The Case for Good Jobs, Zeynep Ton lays out the key findings of years of research spent analyzing companies like Sam’s Club, Quest Diagnostics, and several factories, restaurants, retail stores, and call-fulfillment centers. Her main finding is that investing more in one’s workforce is more cost-effective than investing the bare minimum or a “lean” amount. In addition, customers and shareholders benefit significantly when workers are supported.

In other words, if you want to know how satisfied the customers are, look at how satisfied the employees are. Dick’s has 3.8 stars on GlassDoor, Foot Locker has a 3.7, and REI has a 3.9, well below Fleet Feet (also a chain, albeit run by local owners), which has 4.3. The first store to have Hoka’s in the US was in Boulder. In other words, stores where the staff is more likely to care about service. I know Glassdoor is not a perfect measure of employee satisfaction, but it’s not a bad proxy.

For products that require customers to invest more thought, understanding is crucial. It’s akin to a gradual process. Before introducing your product to the market, ensure that a group of customers truly grasp its value.

However, there’s another aspect to consider. Store associates must be aligned with the brand. Given the tight profit margins for both the manufacturer and the stores, achieving the right balance is critical. If the store staff isn’t enthusiastic about the product, they may dismiss it as another passing trend. This can lead to excess inventory, which can harm the brand’s reputation.

The key trade-off here is deciding whether to collaborate with large retail chains or pursue a direct-to-consumer (DTC) approach. Partnering with big chains provides access to a significant distribution channel, but it may result in a lack of brand recognition. Moreover, it requires substantial inventory and capital management. On the other hand, going the DTC route demands substantial investments in marketing. Both options present challenges.

Now, speaking of scarcity - does it make our hearts race? Oh, absolutely! Think of those elusive Alphaflies – their hard-to-get game is on point. But it’s not just the thrill of the chase. If you want to tango with the big brand beasts, you need more than a unique step. You need your store associates and customers to wholeheartedly feel the beat of your value proposition. It’s a marathon, not a sprint, and Hoka seems to be in it for the long haul.

Loved this deep dive. Hoka has been a fascinating brand to watch so great to peel back the curtain on their strategy.

As always, this was a great way to absorb so many interesting messages.

I first tripped over Hoka when buying arch-support footwear for my nephew post-Covid in Hanover NH at a tiny local running store. I had never heard of the brand, but the sales-person expounded the history of the brand, and the research and production of the sole.