How did COVID (Really) Shape Supply Chains?

As the number of COVID cases around the world is increasing, it's time to revisit the question of what the pandemic’s true impact on supply chains was.

This also comes at the heels of multiple news articles regarding recent changes that are coming into effect. For example, Bloomberg just published an article that states:

“Mexico has emerged as one of the winners from the US-China standoff.

As its giant northern neighbor seeks to cut reliance on its geopolitical rival, investment in Mexico from the likes of Tesla is booming. And in July, Mexico even eclipsed China as the US’s biggest trade partner, regaining a title it held before the Asian country’s ascent.”

In this newsletter, we’ve often discussed about what firms were planning to do and what they did, but this was based on what they said they were planning to do versus what they said they did:

The world “said” is crucial here.

Recently, a group of researchers across several universities, including my colleague Morris Cohen, Vinayak Deshpande (whose papers I’ve mentioned several times), and Shiliang Cui , wrote a paper, trying to understand what changes firms actually made, and to what extent they can be attributed to COVID.

Recap of the COVID Supply Chain Saga

During the COVID-19 pandemic, global supply chains were disrupted both by demand and supply shocks, causing cascading effects on economies and businesses around the world. Demand shocks emerged as consumer behavior shifted drastically and panic buying led to sudden and unprecedented demand for specific goods like sanitizers, masks, and non-perishable foods. Meanwhile, sectors like travel, hospitality, and luxury goods experienced sharp declines in demand due to lockdowns and altering consumption patterns. At the same time, supply shocks were triggered by factory shutdowns, labor shortages, and transportation disruptions in major manufacturing hubs, causing delays and shortages of essential goods. These factors, combined with trade restrictions and geopolitical tensions, exacerbated the fragility of global supply chains. The pandemic underscored the need for supply chains to be more agile, resilient, and diversified to mitigate the impact of such unforeseen shocks in the future.

For those who have forgotten the supply chain horror stories during COVID, these are the three main types of disruption supply chains went through in the context of pandemic outbreaks:

Lockdowns of manufacturers caused a supply disruption in global value chains.

The unavailability of input materials due to a shift in resource allocations toward the healthcare sector impacted companies’ supply.

The pandemic caused issues in global logistics operations as transportation became subject to lockdowns.

While a lot of anecdotal stories emerged regarding what firms did and how they planned to change (and some changed) their supply chain, data to support the notion of what firms actually did during COVID was scarce.

Most of the current research studying the effects of COVID-19 either relies on qualitative information or focuses on quantitative analyses of individual firms. As far as I know, no research has yet embarked on an expansive quantitative exploration of supply chain shifts spanning a broad range of companies and sectors. The paper I mentioned above, uses the extensive Panjiva dataset, which captures every sea-based import to the U.S. since 2016, and offers insights into company-specific advancements and broader industry trends. In particular, it sheds light on the various global supply chain tactics that companies adopted in the wake of the COVID-19 crisis.

The three main questions that the paper tries to address are:

Did firms change their supply chain network structure?

Did firms change their behavior (ordering quantity, frequency)?

To what extent were these changes driven by COVID-19, rather than following general trends of decoupling that started before COVID-19?

Supply Chain Structure

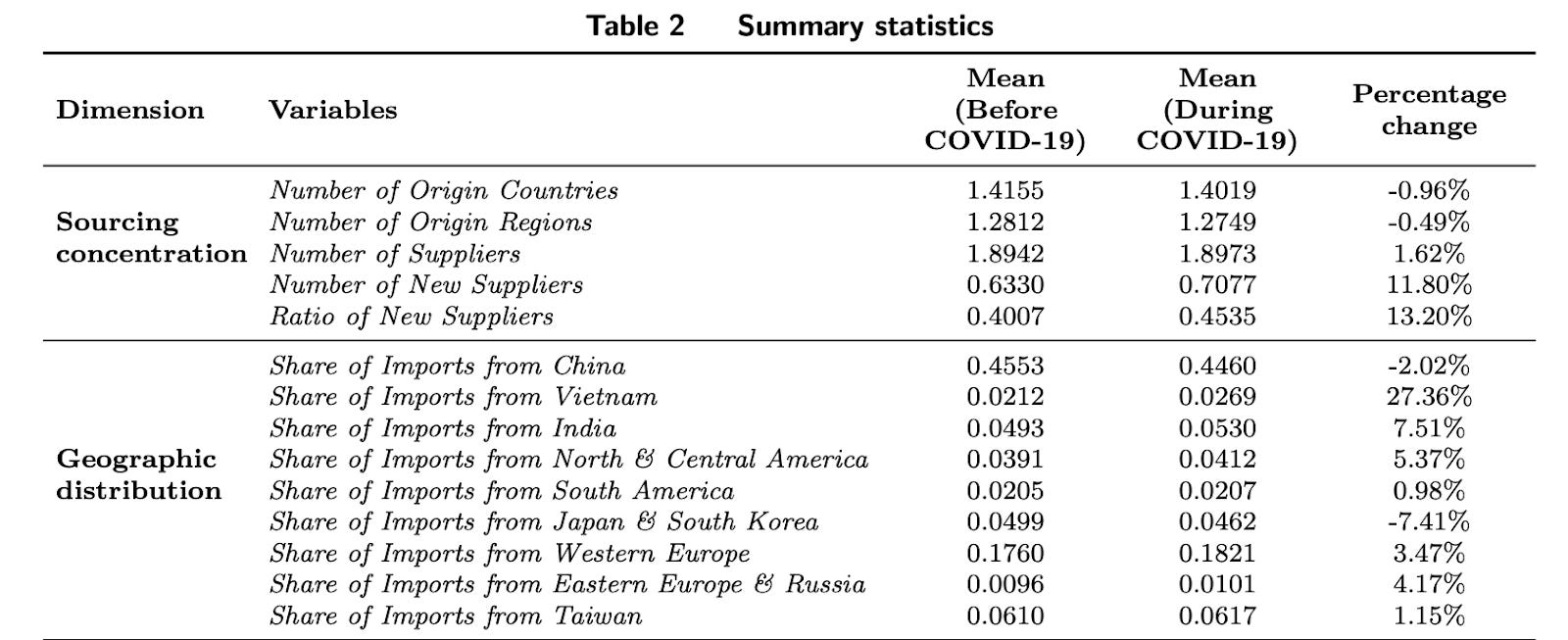

The most interesting result in the paper is the notable drop in the number of countries from which U.S. companies procure their supplies.

But according to the paper,... even with this narrowing down of locations, the number of suppliers that U.S. importers use, doesn’t budge. That is, the total supplier count per company remains stable…

But … there is a rise in both the count and proportion of new suppliers.

The following table summarizes the results:

To provide a more concrete example, let’s look at one of the firms the study focuses on, Honeywell.

Before COVID, Honeywell was pulling in materials from 44 diverse nations right into the heart of U.S. ports. By 2021, that number had dwindled to 37 —Pakistan, Turkey, and Brazil were taken off the list, while others increased their presence. An intriguing observation is that back in 2019, a mere 5% of Honeywell’s seaborne imports hailed from India, and by 2021 that number had doubled to 10%.

Similar results are provided for Ralph Lauren, where the shifts were even more dramatic. In just a span of two years, they ramped up their imports from Cambodia, from 1.27% to a whopping 34.58% of total import weights. And here’s a nugget that caught my eye: in 2021, almost 40% of their direct imports came from brand-new sources, seemingly in a bid to lessen their reliance on China.

Finally, look at Boeing. In 2019, the bulk of imports flew in from China. Fast forward to 2021, and they slashed them by half in terms of weight. And who stepped up to the plate? Canada. Even so, Boeing’s trade with other Asian nations, except China, remained steadfast.

It’s really fascinating to see how these business behemoths navigated the changing tides. These are not firms that are quick to respond to anything, and yet, they restructured their supply chains in times of great peril.

The Drivers Behind the Results

Let’s start with the obvious: None of these decisions is very intuitive. Decreasing the number of countries during times of extreme volatility while keeping the number of suppliers the same, all while onboarding new suppliers, hints at the several tradeoffs that these firms were facing.

When is diversification the right thing to do?

On the one hand, businesses understand the importance of having backup plans, especially when it comes to the origin of their products or materials. This idea of spreading out their suppliers is termed “supplier base diversification.” Using multiple vendors and locations is a protective measure so a company doesn’t have to rely on a single source for materials or products. That way, if one supplier encounters issues, the firm doesn’t risk the entire operation collapsing since there are alternative sources to tap into.

So, when does this not apply anymore?

In situations where suppliers are interconnected — where one supplier might rely on another — a better strategy may be that the main company ensures their direct suppliers are reliable and have their bases covered rather than spreading their own sourcing thin. The same is true for locations. It’s better to ensure the countries the company relies on are safe and resilient rather than reel in more countries and create noise.

A company’s decision whether to diversify its supply sources often hinges on how much it knows about potential risks regarding each supplier. If a company is aware of possible disruptions or challenges a supplier might face, they’d be more inclined to have multiple sources. The fact that firms chose to reduce the number of countries means that the second force is stronger. Having too many unreliable countries in a supply chain makes managing them and the connections between suppliers too unpredictable, and thus counterproductive.

The most notable aspect of the emerging supply chain structure was that it wasn’t about eliminating risky suppliers, but risky countries. Why? Because decisions like lockdowns or closing borders, were made by the governments of these countries, and affected every supplier within that region. So if a company relied heavily on suppliers from a country that went into lockdown, it would be in trouble. In that sense, the smart thing to do was to spread out their supply sources, focusing on different countries, not just different suppliers. All this while keeping the number of suppliers the same.

One of the most interesting parts of the results is the decline of China, even before the more recent trade despises. A lot of U.S. businesses import goods from China. In 2020, almost 19% of everything the U.S. imported came from China. Even more surprising is the fact that over a third of the products that U.S. companies listed in a particular study were sourced solely from China. Given these numbers, it might seem logical for companies to consider importing from other countries to spread their risk.

To conclude this part, I will say that in light of the article I mentioned above, where firms claimed that they planned to on-shore but then admitted they didn’t, it’s interesting to note that this doesn’t mean that they didn’t change their structure. Although they didn’t re-shore, they did modify their supply chain network.

And this is an important result because it shows that globalization is not dead. It just morphed into a more concentrated network. This is consistent with previous articles I’ve written, but with the additional insight that the main concentration happens with countries, not suppliers. Decoupling is real.

Ordering Patterns

So firms changed their supply network structure —fewer countries, same number of suppliers. Did they also change their behavior?

The paper shows that both the weight and volume of shipments have seen an increase. However, these were accompanied by a drop in how often these shipments are made. The result is, of course, a higher level of inventory (which is not reported in the paper but has been observed otherwise). The numbers: post-pandemic data reveals that shipments now contain 9.12% more units, and have 3.3% more volume, but their frequency has decreased by 2.2%.

And a possible explanation would be that akin to people bulk-buying toilet paper at the first hint of a crisis, the bullwhip effect doesn’t rear its head with demand spikes; supply shortages can be culprits, too. When supply seems scarce, companies don’t just fret—they bulk order. Remember the aftermath of the Great East Japan Earthquake in 2011? Firms started hoarding inventory like squirrels preparing for winter. A glaring testament to these turbulent times were the sky-high container freight rates amidst the pandemic. With a shipping squeeze, it’s as if importers played a game of “wait and bundle,” postponing their orders until the coast was clear.

Also, as the cost of ordering increased (driven by the increased shipping cost), you expect exactly this: larger batch sizes with less frequent orders, as indicated by our … EOQ formula.

But it’s important to highlight, yet again, that this is not necessarily an intuitive reaction. And indeed, not every protagonist in our supply chain saga went for the “go big or go home” approach. Diversifying their supplier list, some companies opted for a sprinkle of smaller yet more consistent deliveries. Think of it as choosing a series of short, exciting chapters over one lengthy story. This agility can be a boon, especially when demand becomes as unpredictable as a plot twist.

Is This Even Related to COVID?

One of the most important questions is: How do we know that this really is due to COVID-19 and not just a general trend?

The authors show that “a higher number of cases in a company’s supplying countries is associated with fewer origin countries, a higher share of new suppliers, and with less frequent, but larger shipments.”

I think this is one of the most interesting aspects of this paper. Whether these were plans that existed before and were simply executed and accelerated during COVID, or whether they were completely new realizations among firms, is less clear. But one thing is clear: COVID had a real impact on supply chains —both in terms of structure and in terms of elevating supply chain discussion to the country level.

Businesses now look beyond issues they have with individual suppliers, and consider the risks associated with entire countries. While it would’ve been in their best interest to do this from the start, now there really is no doubt. Before COVID, a company would worry about things like their supplier going bankrupt. But with COVID, new worries popped up, such as entire countries closing their borders or implementing trade restrictions. And this isn’t just about COVID. Geo-political pressure and climate issues are all risks at the regional-country level. The spotlight is now on avoiding countries that might be seen as risky rather than dodging individual suppliers that could be problematic.

Overall, a very fascinating research paper that shows that things are moving. Slowly but moving.