Resilience vs. Economies of Scale in the Modern Supply Chain: A Case Study on the IV Fluid Crisis and Climate-Induced Vulnerabilities

This Week’s Focus: IV Fluid Shortages and the Problem with Concentrated Supply Chains

The current IV fluid shortage, caused by Hurricane Helene, demonstrates the vulnerability of concentrated supply chains in critical industries like healthcare. The combination of low profitability, high regulatory barriers, and a concentrated market structure has made the IV fluid supply chain vulnerable for years, but the extreme weather events have brought more attention to the problem. This week, we take a closer look at the supply chain structure of IV fluids, and talk about risk management frameworks and supply models that may help build resilience next to economies of scale.

During the last few years, particularly since COVID-19, every supply chain (and non-supply chain) executive has been discussing the need to build more resilient supply chains.

For example, Baxter wrote on their website:

“‘COVID-19 made clear that the supply chain innovations we are implementing are essential to maintaining resiliency of our product supply,’ said Jim Borzi, senior vice president and chief supply chain officer at Baxter. ‘We have assessed every aspect of the supply chain ecosystem, created a plan A, B and C should unfortunate disruptions occur, and reimagined seemingly small details. This continuous practice improves our ability to deliver lifesaving and life sustaining products to our customers and the patients they serve.’”

But until the next pandemic, there will be a few hurricanes… so we can test these “new, more resilient” supply chains.

So, how well did one of the most critical supply chains do?

Not well.

Not well at all.

The IV fluid shortage caused by Hurricane Helene’s impact on Baxter International’s Marion, North Carolina plant exemplifies the fragility of concentrated supply chains.

This incident has escalated into a national crisis, jeopardizing regular hospital operations and critical procedures that rely on intravenous (IV) solutions.

In today’s article, we’ll dissect the IV fluid supply chain, the decision-making frameworks at play, and the inherent vulnerabilities driven by a reliance on economies of scale. We’ll then build on risk management frameworks and supply chain models, diving into both theoretical and practical approaches to resilience and scale economies.

Let’s delve in.

The IV Fluid Supply Chain: Anatomy of a Critical System

The IV fluid supply chain is a specialized segment of the healthcare industry, tightly concentrated in terms of production facilities and manufacturers. Only a handful of companies dominate the market, with Baxter International and B. Braun holding significant shares. Baxter’s North Cove facility in Marion, North Carolina, supplies 60% of the United States’ IV fluids, while B. Braun operates another essential plant in Daytona Beach, Florida. Together, these companies are responsible for most IV solutions delivered to hospitals nationwide.

The production of IV fluids is a highly regulated process due to the sterile nature of the product —critical for both patient hydration and drug administration. Facilities, like Baxter’s Marion plant, are required to maintain high standards of cleanliness and reliability, as any contamination could lead to severe harm in patients. These plants are typically located in regions that offer cost advantages, such as lower labor costs and favorable state taxes, which often explains their geographic concentration in the southeastern United States.

However, this concentration introduces systemic risks. Hurricane Helene flooded the Marion plant, breached a nearby levee, and damaged the bridges connecting the site to distribution networks.

As a result, hospitals across the U.S. were forced to delay elective procedures and conserve IV fluids by turning to alternative methods like oral hydration and manual syringe-based drug delivery. Given the complexity of resuming full operations at such facilities, the shortage is expected to last for months.

IV Fluid Shortages: A Longstanding Issue Before Helene

While Hurricane Helene may have thrust the issue of IV fluid shortages into the spotlight, it’s not new. According to NBC News, the U.S. has been dealing with chronic shortages of critical IV fluid for years, and the recent damage to Baxter has only exacerbated an already fragile supply chain.

The FDA reports that saline solution has been in shortage since 2018, sterile water since 2021, and dextrose solution since early 2022. Both economic and structural factors in the IV fluid supply chain are to blame.

The shortage crisis reached a tipping point with Hurricane Helene, which “...damaged a Baxter International plant in North Carolina, triggering additional shortages of dextrose solution, an electrolyte solution called lactated Ringer’s, and a peritoneal dialysis solution. Currently, hospitals are getting about 40% of their normal shipments,” reports NBC News.

Efforts to alleviate the shortages have been made at the federal level, with President Biden invoking the Defense Production Act to prioritize resources for Baxter to clean and rebuild its facility. Additionally, the FDA is allowing Baxter to temporarily import IV fluids from its plants in Canada, China, Ireland, and the U.K. However, as experts warned, “the long-term shortages will persist unless there is a guarantee of long-term profits for companies from IV solutions.”

Decision-Makers in the IV Fluid Supply Chain

To better understand how such a high concentration occurred, we must first understand the supply chain’s structure.

The decision-makers involved in the IV fluid supply chain span various stakeholders, each with different priorities:

Manufacturers (e.g., Baxter, B. Braun): These companies prioritize cost efficiency to remain competitive, given the slim margins in the medical supplies market. Economies of scale often drive decisions to concentrate production in a few large plants. They also invest in ensuring high quality in terms of compliance and sterility.

Healthcare Providers (hospitals, clinics): Healthcare providers depend on the reliable supply of IV fluids for a wide range of treatments, from hydration during surgeries to drug administration for chemotherapy patients. When a disruption occurs, these providers are tasked with developing workarounds and contingency plans to minimize the impact on patient care.

Regulatory Agencies (FDA, ASPR): The Food and Drug Administration (FDA) and the Administration for Strategic Preparedness and Response (ASPR) are responsible for ensuring that the healthcare supply chain is resilient enough to handle disruptions. These agencies also regulate the production of sterile fluids and can expedite approvals for alternative suppliers, or extend expiration dates for existing supplies. It’s very clear that the agencies prioritize quality over resilience.

While I absolutely understand the need to ensure high quality and compliance for these products, we must acknowledge that strict regulations make it difficult for new entrants to compete, resulting in further concentration of production, and a less resilient supply chain.

Group Purchasing Organizations (GPOs): GPOs like Premier Inc. are critical in negotiating bulk purchases of medical supplies for hospitals. They track shortages and facilitate alternative sourcing strategies when supply chain disruptions occur, as evidenced by their reporting that 86% of health providers were already experiencing IV fluid shortages after the hurricane.

The industry’s structure encourages the concentration of production in a few large plants due to the capital-intensive nature of manufacturing sterile medical supplies. From an economic perspective, this industry operates under extremely high fixed costs, stemming from investments in sterile environments, regulatory compliance, and advanced technologies needed to ensure product safety. It’s clear that industries with such high fixed costs benefit disproportionately from economies of scale, where average costs per unit decrease significantly as output increases.

This creates a strong economic incentive to maximize production capacity utilization, consolidating operations into fewer, larger facilities. By doing so, manufacturers can spread their fixed costs over a bigger production volume, achieving a lower average cost per unit. Additionally, the stringent regulatory standards set by agencies like the FDA further encourage this consolidation, as each facility must adhere to costly regulatory requirements, and when concentrated in fewer locations, this process is easier to manage. In contrast, to meet similarly high standards, a more resilient, decentralized supply chain would require multiple plants, driving up costs significantly due to duplication of infrastructure and regulatory compliance. This leads to a classic trade-off between cost efficiency and risk mitigation. Supply chain theory, particularly models like the newsvendor model, further emphasizes that firms in industries with low-profit margins and high fixed costs are often more focused on minimizing costs rather than building redundancy into their supply chain. Consequently, the cost-benefit analysis skews heavily toward centralization and scale, even though this increases vulnerability to disruptions.

Moreover, market forces and competitive pressures significantly reinforce this behavior in industries like pharmaceuticals and medical supplies. Because products such as IV fluids are often sold at razor-thin margins and bundled with other medical products, firms are compelled to keep production costs as low as possible to remain competitive. This creates a structural bias toward concentration rather than diversification, even if resilience is sacrificed.

Risk Management in the Face of Supply Chain Vulnerabilities

In light of these increasing risks, supply chain scholars have developed frameworks to help firms mitigate disruptions. The paper by Wang, Gilland, and Tomlin titled “Mitigating Supply Risk: Dual Sourcing or Process Improvement?” examines the effectiveness of two different supply chain risk mitigation strategies: dual sourcing (sourcing from multiple suppliers) and process improvement (enhancing the reliability of a single supplier).

The paper’s primary research question is: How can firms best mitigate supply risks through either dual sourcing or process improvement? The authors explore which conditions favor either of these strategies and whether a combined approach can provide additional value.

The authors’ motivation stems from increasing concerns over supply chain reliability, just like the IV fluid case. Many firms experience supply disruptions due to unreliable suppliers, leading to lost revenue and operational inefficiencies. Previous studies have focused on using dual sourcing to mitigate risks, but this paper brings attention to the less-studied option of directly improving a supplier’s reliability. This issue is especially critical in industries where supply disruptions have high costs, such as the IV fluid supply chain, where disruptions affect patient care.

The authors use a mathematical model based on the newsvendor framework to study a firm procuring from unreliable suppliers. They consider two types of supply uncertainties: random capacity (limited ability to produce) and random yield (unpredictable output quality), and analyze how a firm can mitigate these risks.

To put these two strategies in the context of the IV fluid supply chain:

Dual Sourcing: Firms source from multiple suppliers to reduce reliance on a single production node. For IV fluids, this could mean Baxter diversifying production across multiple plants, or sourcing from external manufacturers like ICU Medical.

Process Improvement: Firms can invest in improving the reliability of a single supplier, becoming more resilient against disruptions. For Baxter, this might involve fortifying the Marion facility against future floods or hurricanes by building more robust flood defenses or improving logistical flexibility.

The study’s implications suggest that while investing in supplier reliability (process improvement) can mitigate risks, the IV fluid industry may benefit more from dual sourcing due to the high variability in supplier reliability during disruptions. Furthermore, the industry’s focus on economies of scale exacerbates its vulnerability by reducing the diversity of supply sources.

Thus, balancing cost efficiencies with resilience through strategies like dual sourcing may help avoid future disruptions. The study indicates that a combined approach—improving reliability while diversifying suppliers—may provide optimal protection in critical supply chains like those of IV fluids.

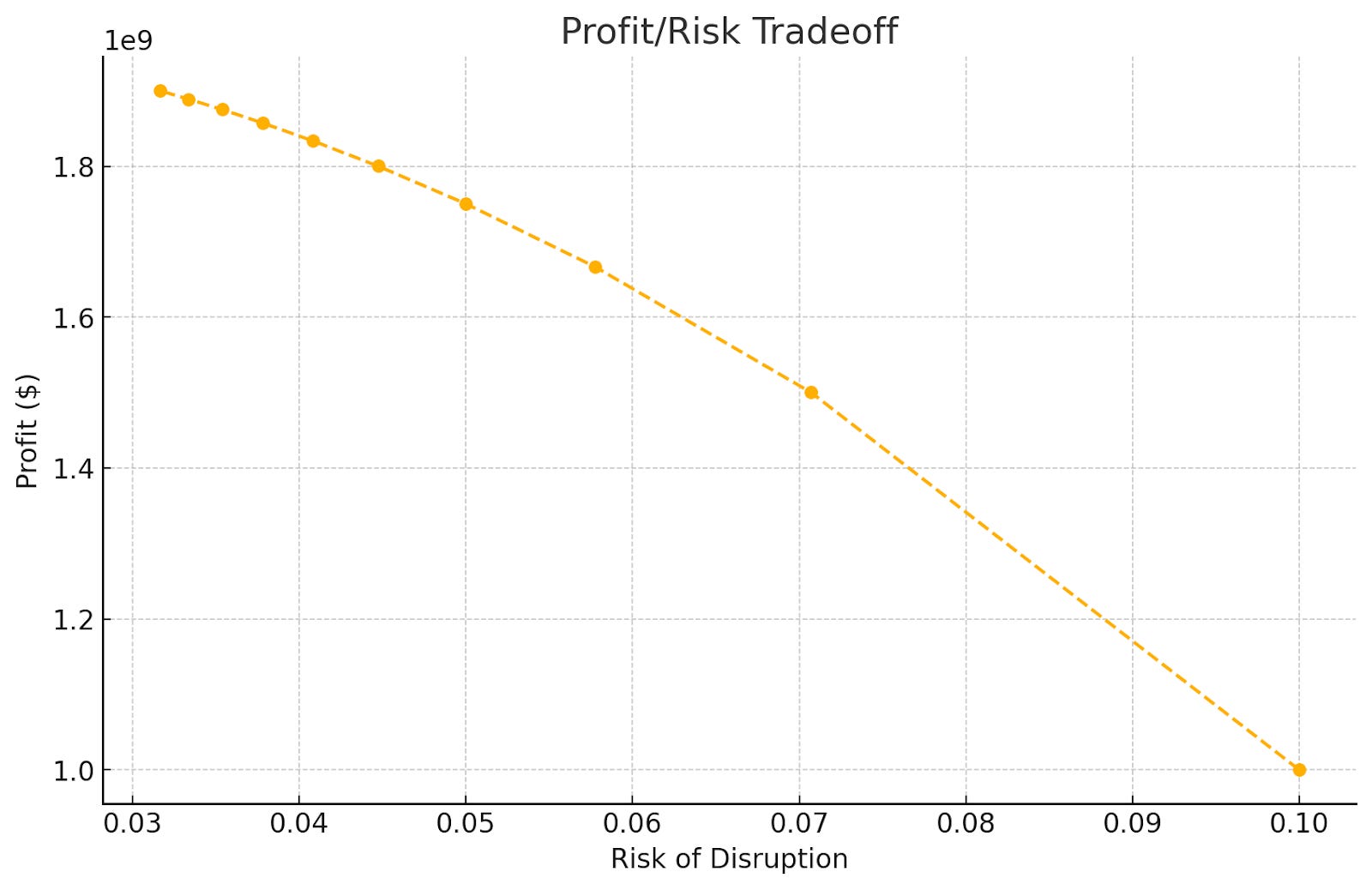

While the paper doesn’t consider more than two suppliers, we can extract that as suppliers increase, they lose economies of scale, resulting in higher costs but a less vulnerable supply chain. A simple model would result in the following tradeoff curve:

The Role of Climate Change in Supply Chain Vulnerabilities

The IV fluid supply chain disruptions exemplify a broader phenomenon: the increasing frequency and severity of supply chain disruptions caused by climate change. As extreme weather events such as hurricanes, tornadoes, and floods become more common, they exacerbate vulnerabilities in highly concentrated supply chains.

The IV fluid shortage is one more example of climate-driven disruptions, which are not just random shocks but are becoming systemic risks that require companies to rethink how they design their supply chains.

The paper “Managing Climate Change Risks in Global Supply Chains: A Review and Research Agenda” addresses the question: How can climate change risks be managed in global supply chains?

The paper aims to explore how risks posed by climate change, such as extreme weather and resource scarcity, impact global supply chains and how these risks can be mitigated. The focus is on understanding the sources, consequences, and management strategies of climate risks in supply chains.

The motivation stems from the increasing frequency of climate change-related disruptions, such as floods, droughts, and hurricanes, which significantly affect industries like food production, transportation, and logistics. These disruptions create cascading threats, which propagate through global supply chains, greatly impacting their resilience. The paper highlights the limited research on climate change in the supply chain context, calling for a more systematic understanding of how supply chain risk management (SCRM) can integrate climate change.

The paper finds that climate change and supply chains influence each other: supply chains contribute to greenhouse gas emissions, while extreme weather conditions disrupt supply chains. The identified risks include disruptions in transportation, natural resource scarcity, and higher costs.

The paper proposes several proactive and reactive strategies, including carbon footprint mapping, eco-innovation, green sourcing, and policy compliance. The study emphasizes that most risk management approaches are proactive but must be integrated with adaptive strategies to respond to unpredictable disruptions.

Regarding the IV fluid supply chain, the findings imply that the concentration of production in a few large-scale facilities is vulnerable to climate change risks, such as hurricanes (e.g., Hurricane Helene). The lack of resilience in this supply chain structure is a critical risk, as climate-related disruptions could lead to shortages in vital medical supplies. The paper suggests that a more decentralized supply chain structure, which incorporates strategies like diversified sourcing and environmental risk management, would help mitigate such risks.

As climate change accelerates, these trade-offs will become more pressing. Extreme weather events are predicted to increase both in frequency and severity. This presents a growing challenge for highly concentrated supply chains that rely on a few production nodes.

Industries will need to re-evaluate their reliance on economies of scale and consider resilience-focused strategies. Companies may need to adopt dual-sourcing or geographically diversified production facilities to mitigate the impact of climate-induced disruptions. Regulatory bodies and healthcare providers must also advocate for supply chain decentralization to protect against future shocks.

Conclusion

The vulnerabilities of industries with concentrated supply chains (like the IV fluid) will only grow —a fact that should force companies to rethink their strategies. Firms like Baxter must weigh the benefits of economies of scale against the pressing need for resilience. Regulatory bodies and healthcare providers should advocate for supply chain diversification and risk mitigation strategies to prevent similar crises in the future. By adopting a more distributed production model and investing in dual sourcing or process improvement, firms can better safeguard the continuity of essential medical supplies, ensuring that future natural disasters do not lead to life-threatening shortages.

The damage caused by Hurricane Helene merely exposed a pre-existing weakness. Such shortages will likely continue if the underlying economic drivers are not addressed, and manufacturers’ long-term profitability is not achieved.

As climate change continues to increase the frequency of extreme weather events, companies across all sectors must embrace risk management frameworks, prioritizing resilience as much as cost efficiency. The time for incremental adjustments has passed. Proactive, structural changes to supply chain strategies are necessary to ensure stability in the face of future crises.

Hi Gad, this is not new. A very similar issue happened in 2017 when Maria hit Puerto Rico. https://www.baxter.com/perspectives/community-engagement/global-response-hurricane-maria

And previously with FDA warning letter to the Hospira manufacturing site the same year - a single warning letter to one of the suppliers can severely affect the whole supply chain.

This is unlikely to change as Health Systems and GPOs don't want to pay higher prices for increased reliability in supply and the IV fluid manufacturers are pressured to deliver earnings to Wall Street. There's no incentives for any party to reduce the risk.

Temporary importation from manufacturing sites across the world seems to be a reasonable approach to solve for these types of cataclysmic events. It seems that's the temporary solution being implemented. Although I agree that it would be ideal to have a better solution for this.

I have personal experience in multiple adjacent businesses at one of the manufacturers you mention.

The fundamental challenge is that customers -- health systems and GPOs negotiating for them -- are completely unwilling to pay anything for increased reliability. This is a classic prisoner's dilemma in which neither major firm can afford to invest in capacity without losing share or suffering lower margins than its competitor.

As a result, prices are low. IV solutions produced so cleanly that they can be infused directly into veins sell for less per oz than bottled water at a convenience store.

The start-up costs to build a plant, both in terms of capital and regulatory requirements are not so onerous that they prevent market entry. In fact, I'd say that the regulatory barriers are immaterial to this analysis, especially as there are many firms that produce equivalent products (generic drugs in a bag) but not IV solutions or that produce IV solutions, but not at scale for the US market.

Because prices are low and aggressive price competition between Baxter and Braun would make the market unprofitable for both, both firms sell IV solutions as part of a bundle negotiated with GPOs. At a high level, the best price of something a hospital really wants (e.g. an expensive IV pump) is only achieved by committing to buy 80% or more of the IV solutions business from the same manufacturer. This scheme is what prevents market entry by making the prospect of gaining share unlikely for any new entrant. But the root cause is the lack of profitability in the category.

Two other barriers to increasing supply are significant, but secondary.

- The long-term trend for this market is slight reduction. I'm too far removed to have current data. But the general trend of treating more patients as outpatients in the hospital (versus multi-day inpatient stays) or outside of the hospital completely has put downward pressure on IV solutions demand, even though an aging population and increase in some conditions is a positive. As a result, no IV solution plant expansion is going to make the top 10 capex investments at any company.

- Bags of water are really heavy. At IV solutions prices, it's not profitable to manufacture these products OUS and ship to the US. This dynamic makes the business case for having multiple US plants easier to make, but low margins in this category and the lack of market growth make that argument moot.

Finally, lest we think this is specific to IV solutions, it's not. When patient deaths were linked to adulterated heparin many years ago, the root cause was Chinese "API" (the drug itself) suppliers who were making adulterated product to save money. Manufacturers explored the market for higher-priced products with increased controls over the supply chain, including US-manufacturing, but hospitals were similarly unwilling to pay a premium for those.

Absent government intervention, this is an unsolvable problem.