What happens When Amazon Buys Too Much Prime Space

When serving as Amazon’s CEO, Jeff Bezos liked to advocate for managers within Amazon to make decisions that were easy to reverse. He would call these decisions “two-way doors.”

This may be possible when launching a new feature, trying a new payment method, or launching a new product (such as Kindle, Fire, etc.), but it’s much harder when it comes to physical infrastructure. Buying real estate and building warehouses are decisions that cannot be easily undone.

So what do you do when you realize that some of these aggressive investments were a bit too aggressive?

This is precisely where Amazon finds itself over the last few days when the firm announced that it over-invested in capacity and, at the same time, launched a new offering (maybe even a new business model) aimed at utilizing this exact excess capacity.

Too Much Space

After last week’s statement: “We have too much space right now versus our demand patterns,” Amazon’s CFO, Brian Olsavsky, continued to tell reporters:

“We’ve come out of a very tumultuous two years…We are glad we made the decisions we made over the past two years. And now we have a chance to right-size our capacity to a more normalized demand pattern.”

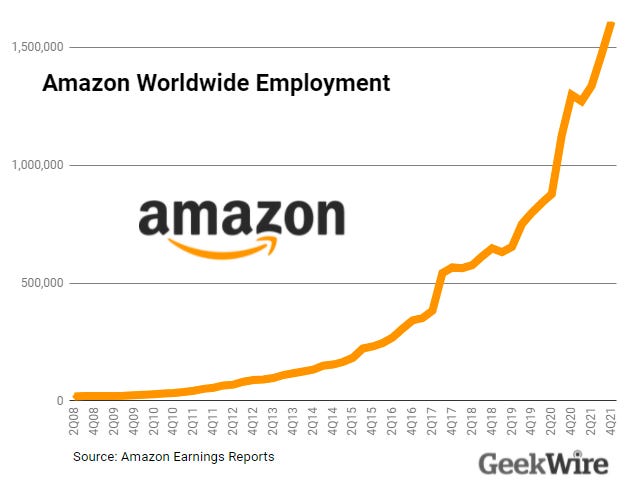

“...Amazon’s CEO Andy Jassy said the year-over-year growth of 39% that Amazon saw in its consumer business during the pandemic in 2020 ‘necessitated doubling the size of our fulfillment network that we’d built over Amazon’s first 25 years — and doing so in just 24 months.’”

And the numbers are indeed staggering:

“Amazon’s fulfillment network and data center facilities (owned and leased, domestic and international) rose from 272 million square feet at the end of 2019 to 525 million square feet at the end of 2021, according to its annual SEC filings.”

And this is far ahead of any other retail competitor:

The distribution network is, of course, only part of a more extensive network of solutions. Over the last several years, Amazon created its own last-mile delivery network, known as AMZL, utilizing a network of dedicated Amazon Delivery Service Partners, and reducing its dependence on delivery companies such as UPS and USPS.

Olsavsky also explained that due to the long lead time required to build such warehouses, the significant increase in demand during COVID, required the firm to act quickly.

But this announcement came after the disclosure that Amazon’s online sales fell 3% for the quarter to $51 billion. Consumers are more comfortable buying in person again now that they feel that COVID is over.

So the demand curve is flattening, and Amazon had to make some decisions.

Buy with Prime

Two weeks ago, Amazon announced the launch of a new program, “Buy with Prime”:

“Buy with Prime will allow millions of U.S.-based Prime members to shop directly from merchants’ online stores with the trusted experience they expect from Amazon—including fast, free delivery, a seamless checkout experience, and free returns on eligible orders.”

While the announcement is seemingly unrelated to the excess capacity disclosure, it clearly has everything to do with it. Similar to what Amazon did with AWS (which was initially created for internal purposes), Amazon is using the fact that it has excess capacity to launch new business lines.

Amazon is already utilizing its warehouse network to lead its FBA (Fulfillment by Amazon) program, which allows third-party sellers to fulfill their orders through Amazon’s platform.

By creating ‘Buy with Prime,’ Amazon aims to extend the program to the brands’ own web stores, and onboards BigCommerce to minimize the real impact, which is, essentially, competing with other SaaS solutions that currently provide the tools for these brands to build their own websites, such as Wix and Shopify. Amazon makes this more attractive by offering the additional (and more significant) advantage of its amazing distribution network. The exact same one that now happens to have a lot of excess space.

Who will be affected or is under attack by this?

Primarily Shopify (which is, of course, not mentioned in Amazon’s announcement).

Shopify has grown extensively over the last few years and has been consistently outperforming Amazon up until its stock started sliding in 2022.

Over the last few years, Amazon forced many of the brands selling on its platform to use the FBA solution, essentially earning fees both on the product sales (referral fees) and on the product fulfillment (inventory and fulfillment fees). For many small brands, there was no other option.

But now, Amazon is utilizing a different strategy, turning to brands that currently do not operate on Amazon (or those who also have D2C websites) and suggesting that they utilize the Amazon network (and the Amazon Prime payment feature).

In my opinion, the main realization within Amazon is that some of the actions taken (for example, launching private label products to compete with best selling products on the platform and providing very limited data to sellers) ultimately pushed many firms off Amazon.com. In fact, the advice for all brands was that if you want to maintain your brand, avoid Amazon.

Amazon is now trying to rectify that, but this move also demonstrates the pressure Amazon is under to continue to grow—and maybe even more now since there is a lot more capacity to fill.

It is clear that Amazon would prefer to sell through its website, allowing the firm to collect data, achieve better margins, and pressure sellers to lower prices (even on their own websites). But Amazon also knows that this will not happen forever, and it is ceding this to the brands. If you don’t want to come to us, we will come to you.

It is still too early to tell how successful this new program will be, but I will say that in my opinion, its impact won’t be as far-reaching as one might expect.

Will it make a dent in Shopify? Absolutely.

Will it convince the big brands to move to Amazon? I'm not 100% sure.

The ‘prime’ reason they're not on Amazon is the fact that they don’t want to create that dependency. Over the years, anyone who has ever done business with Amazon has learnt that as soon as they lose leverage, Amazon uses its bargaining power to extract whatever “receivables” it believes it deserves.

The Downside Effect: Real Estate Bullwhip

But the excess space will also have potentially significant, negative implications, and not only for Amazon.

And since we have all become “experts” in supply chains during COVID, the critical question is whether this will result in a bullwhip effect.

For those who are unfamiliar, the bullwhip effect occurs when an upstream shock gets amplified further up in the supply chain, and its root cause is the presence of a long lead time paired with the inability to determine whether the shock (in this case a significant increase in online purchases due to COVID) is temporary or a long-term consumer behavior change. When you realize that it’s only a blip (or not as persistent as you anticipated), it’s too late for firms to course-correct.

In this case, the fact that Amazon built significantly over the capacity of its warehouses may have a deflationary impact on three sectors: commercial real estate, worker wages, and automation equipment.

Real Estate

Over the last few years, the increased e-commerce activity resulted in warehouse vacancies being close to zero, and, according to reports from Prologis, rent prices spiked to record levels around the world. Globally, rents rose a record 15% in 2021; in the US and Canada, the average rent hike was nearly 18%. Amazon is not the only player in this market, but it is one of the major ones.

Worker Wages

I have already explained how the shortages that many firms faced during COVID, in terms of warehouse and logistics workers, were due to the fact that Amazon and Walmart hired extensively during that time.

And what allowed them to attract so many employees were better wages and promises of tuition benefits. This is most likely going to stop now.

Warehouse Automation

The size of the warehouse automation market worldwide has been increasing steadily since 2012.

But the expectation that it will continue to increase is a little too rosy given that the main player is most likely not going to acquire capacity over (at least) the next year or so.

The Case Against the Bullwhip Effect

But to be honest, I am not convinced this effect is going to be all that significant.

Why?

Amazon has shown a lot of appetite and the “capacity” to launch new business lines on top of long-term capability building.

So the excess capacity will not be dumped on the market, but instead used to generate a whole new set of businesses that will fill the void. This is precisely the point of ‘Buy With Prime.’

But even ‘Buy with Prime’ is going to have a deflationary impact.

It will put pressure on lease prices. It will put pressure on wages.

But it will also put pressure on 3PL firms who have been doing well over the last few years, given the limited number of vacancies and the shortage of warehouse employees.

And it’s going to pressure Shopify and all other payment options available.

Will we, as consumers, benefit from this? In the short and medium-term, the answer is yes: more options and more efficient alternatives.

But we will get to the point where we may be discussing whether Amazon is too big to fail, or whether the pressure it creates will prevent new businesses from emerging by taxing the entire economy. This day is not too far.

I know that Amazon has been working on robots for their warehouses for a long time and already testing them in masses. I think that the suggestions that warehouse automation will not continue to increase is not accurate as Amazon needs to solve for it's current warehouses first, and then some. Wouldn’t be surprised if one day they will create a new business from selling these robots (same as AWS..)